Roof Depreciation Life

Part Three The Value Of Accurate Roof Age In Claims

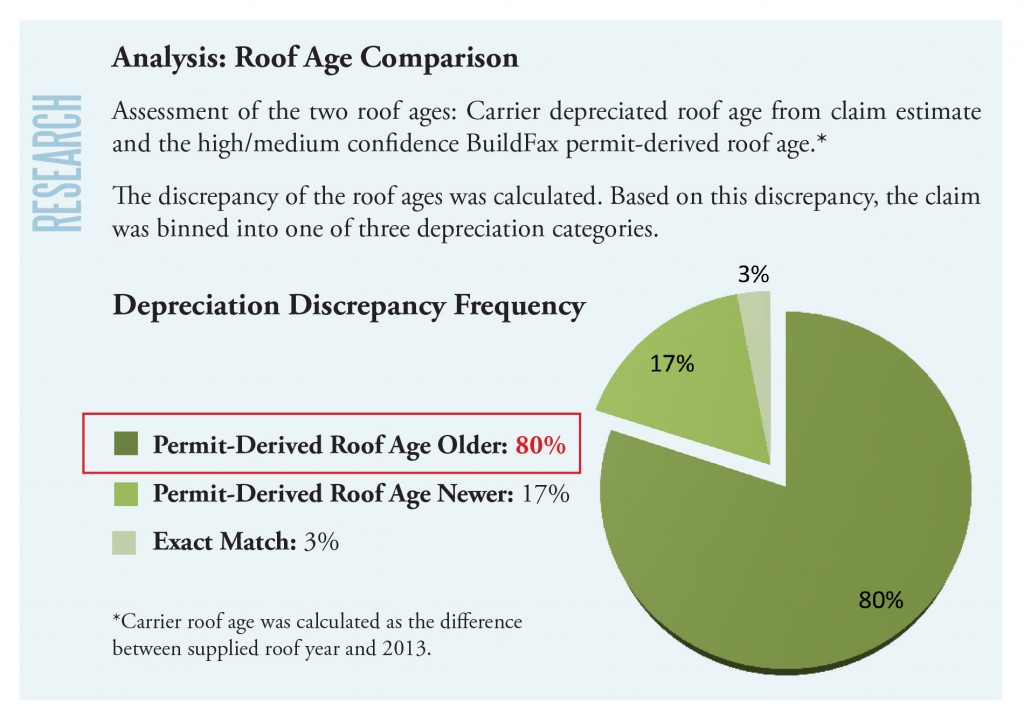

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

What Is The Depreciation Of The Roof On A Commercial Building

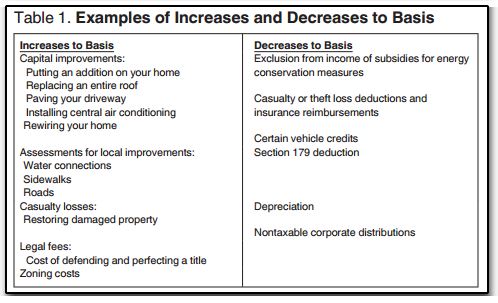

12762 Increasing Basis On An Asset Being Depreciated

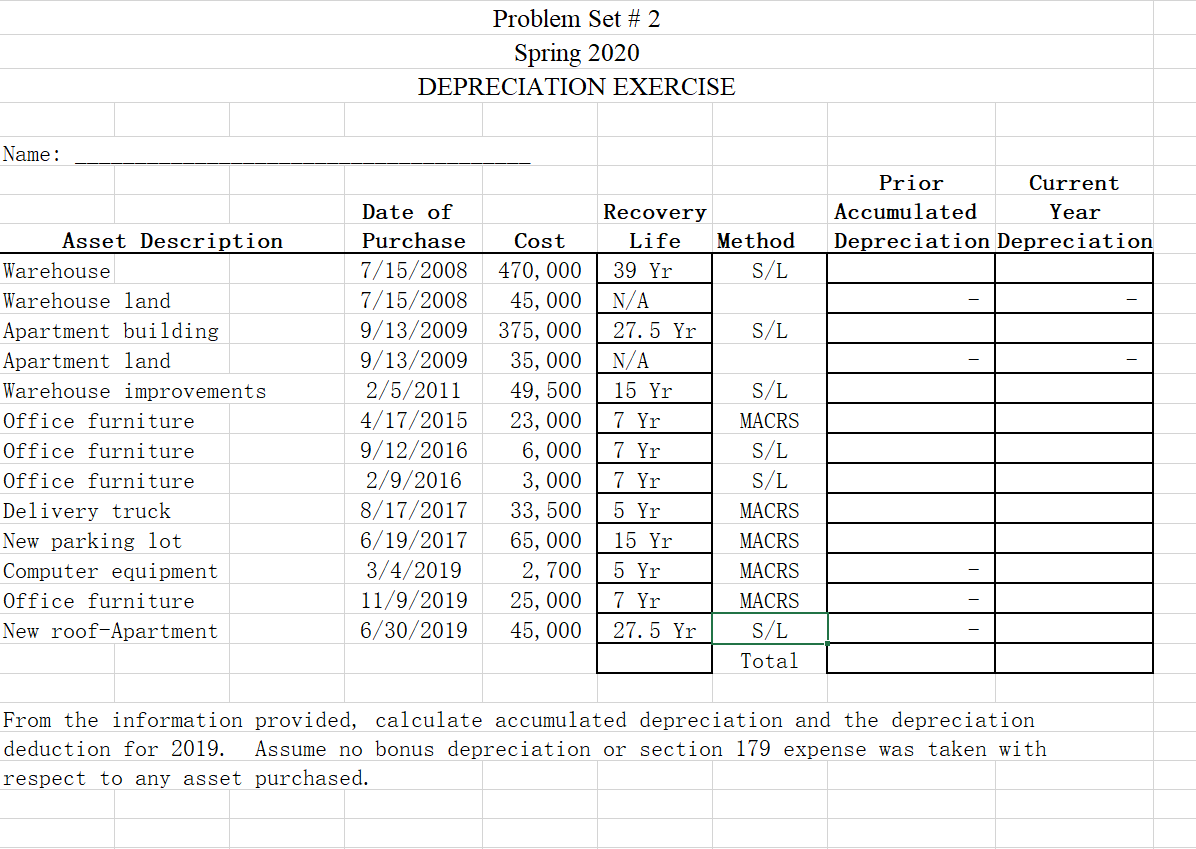

Problem Set 2 Spring 2020 Depreciation Exercise Chegg Com

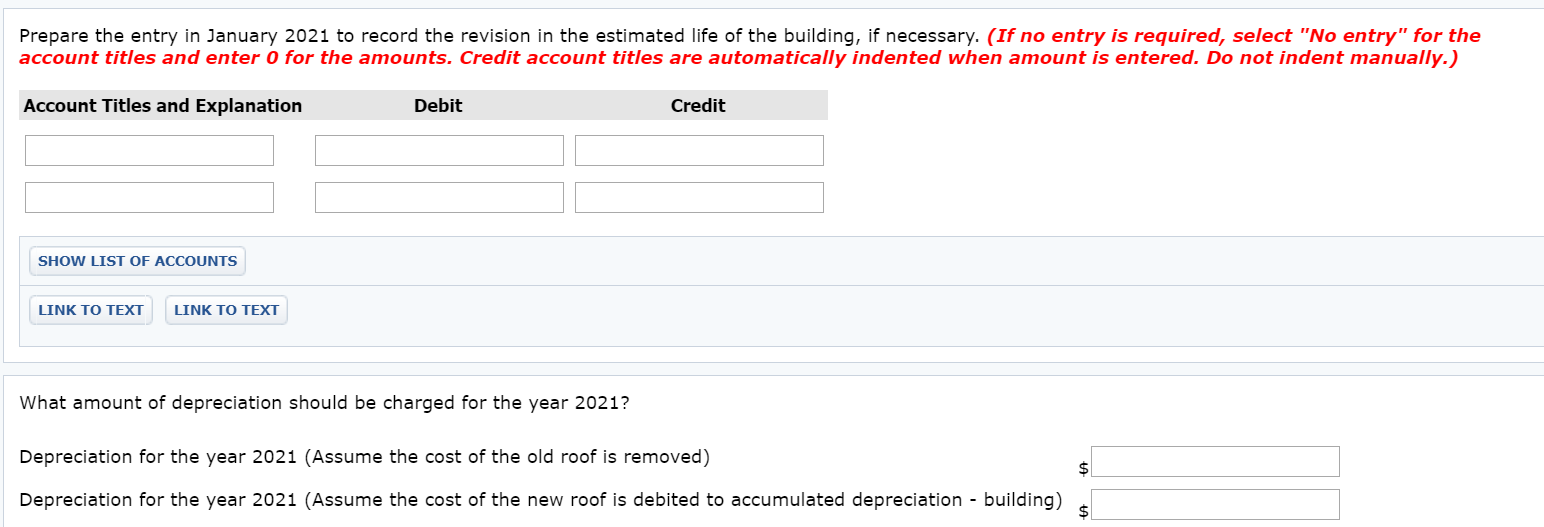

Decide if the new roof is a capital improvement.

Roof depreciation life.

Actual Cash Value The 15 Year Roof Rule Cw Roofing Construction

Guide To Expensing Roofs Expense V Capitalization Section 179 D Kbkg

Rcv Vs Acv Whats The Difference A Young Insurance Agency Inc

Solved Exercise 11 13 Concord Company Constructed A Build Chegg Com

How Rental Property Depreciation Works The Benefits To You

Chapter 14 Cost Approach Cost Approach The Cost Approach Is Most Useful When Property Is Unique Property Is Reasonably New And The Improvements Ppt Download

Rental Property Depreciation Rules Schedule Recapture

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin

Homeowners Insurance 101 Roof Age Matters At Claim Time

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin Insurance Deductible Home Insurance Insurance Marketing

Rental Property Depreciation Reducing Your Tax Burden 37parallel Com

Overview Of The Cost Approach Final Reconciliation Ppt Download

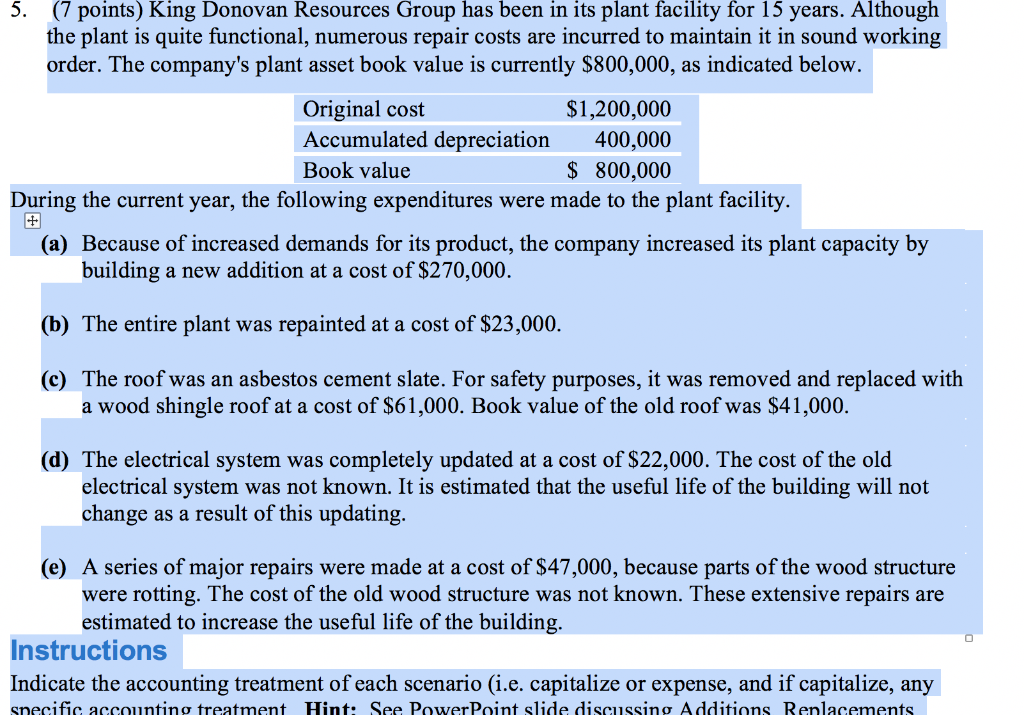

Solved 7 Points King Donovan Resources Group Has Been I Chegg Com

My Roof Needs To Last How Long

Https Www Scoremaine Org Wp Content Uploads 2018 11 Hiatt Msc Tax Cuts And Jobs Act Df 11 18 1 Pdf

Solved A Capital Expenditure Adds To An Asset C Is A Cre Chegg Com

Depreciating Labor Costs The Rough Notes Company Inc

Highland Commercial Roofing Trump Tax Code Effects On Roofing

Understanding Qualified Improvement Property Depreciation Changes Mlr

Roof Deductible L Depreciation L Roof Insurance Claim Specialists Bbr Contracting Residential Commercial Roofing Services

Section 179d Tax Deduction For Commercial Roof Replacements

Depreciation Recapture What Is It And How Can I Reduce It

Roof Insurance Acv Vs Replacement Cost Bankrate

Irs Issues Guidance For Change To Real Property Depreciation Grant Thornton

Source : pinterest.com