Roof Depreciation Life Rental Property

Depreciation Recapture On Rental Property And Calculator Avoid The Painful Irs With A 1031 Exchange Inside The 1031 Exchange

How Rental Property Depreciation Works The Benefits To You

Rental Property Depreciation Rules Schedule Recapture

Understanding Depreciation Recapture Taxes On Rental Property Rental Property Being A Landlord Military Housing

How The New Tax Law Affects Rental Real Estate Owners

Real Estate Investing Frequently Asked Questions Most Common Faqs Real Estate Rentals Renting Out Your House Rental Property

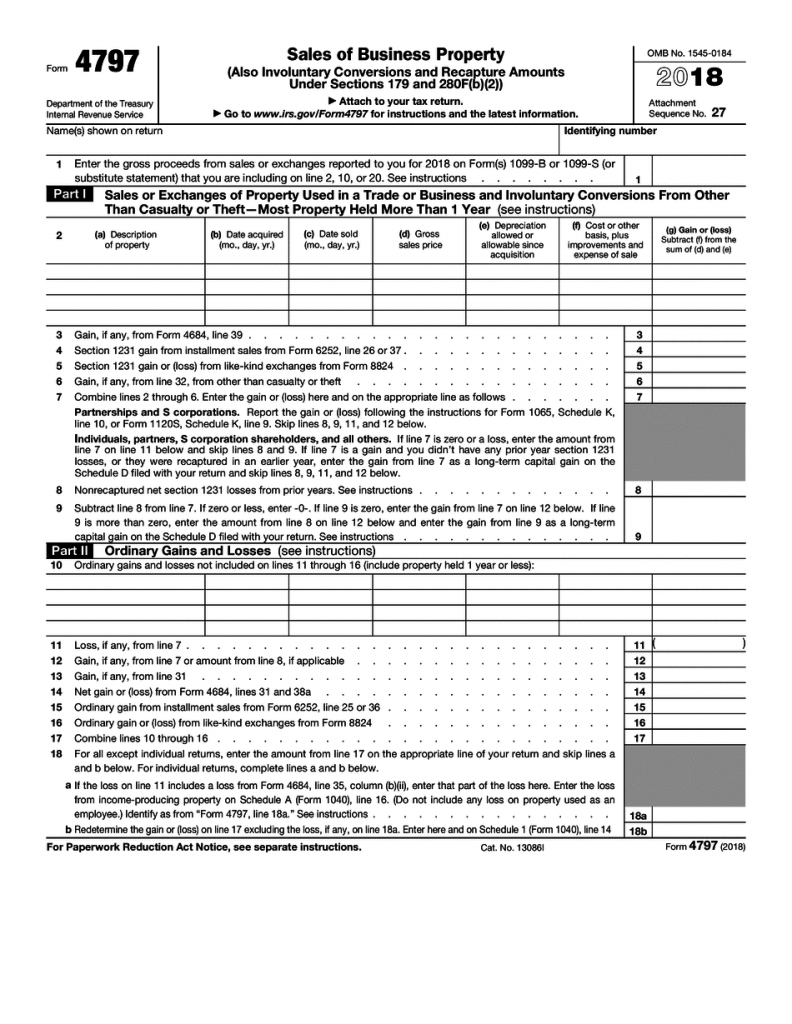

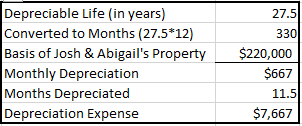

Are generally depreciated over a recovery period of 27 5 years using the straight line method of depreciation and a mid month convention as residential rental property.

Roof depreciation life rental property.

8 Proven Ways To Feel Safe And Secure With Tenants In Your Own Home Landlording Investment Property For Sale Rental Property Income Property

23 Items For Depreciation On Your Triple Net Lease Property Net Lease Tax Deductions Capital Gains Tax

Why Depreciation Matters For Rental Property Owners At Tax Time Stessa

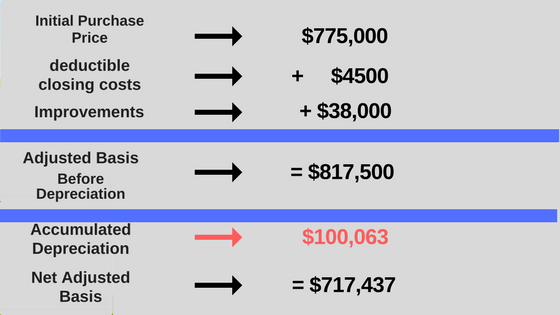

Calculating Your Profit When Selling Your Rental Property Mortgage Blog

Legalaccomplished Rental Property Tax Deductions Worksheet Rentalproperty

Pdf Download The Landlord S Financial Tool Kit Full Pages By Michael C Thomsett

Depreciation Recapture What Is It And How Can I Reduce It

4562 Half Year Mid Month And Mid Quarter Conventions 1120 1120s 4562

Tax Depreciation Schedules Australia One Of The Least Benefit Of Property Depreciation Is That They Are Non Cash Deductions It Means Tax Deduction Legal Rule

Real Estate Tax Depreciation Basics Millionacres

What Is Rental Property Depreciation

Rental Property Depreciation Reducing Your Tax Burden 37parallel Com

Buyer Contact Form Black Real Estate Forms Realtor Forms Real Estate Agents Realtors Real Estate Marketing Active Real Estate In 2019 Real Estate Forms Real Estate Buyers Real Estate Investing

Turbotax Guide To Tax Deductions For Rental Property Depreciation Thestreet

850 Bunker Hill Boulevard Jacksonville Fl 32208 Hotpads Bunker Hill Renting A House Historic Properties

Us Expat Taxes Explained Rental Property In The Us Us Expat Taxes Explained Rental Property In The Us

Jessy Milner And How He Made 86 000 On His First Deal Livin The Dream Epic Real Estate Investing Podcast In Real Estate Education Real Estate Investing

Florida New Construction Rebate Program New Construction House Hunting Checklist Resources For Home Buyers Room Ideas Home Buying Tips Home Inspection

1

Roofing Contract Template 145 Roofing Contract Contract Template Roofing

Pet Care Center Life Petinsuranceplans How To Feng Shui Your Home Buying Your First Home

What If You Forgot To Depreciate Your Rental Property Ipropertymanagement Com

Http Carrstax Com Carrstax Images Rental 20property 20organizer 20worksheet 1 Pdf

Prateek Grand City Bharosa Jyada Prateek Ka Vaada With Images Property Valuation Melbourne City

Source : pinterest.com